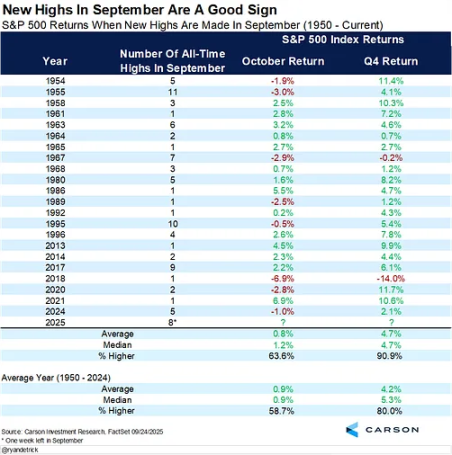

Partial bull markets may become the norm, with market recovery expected in Q4

The bull market may continue for a while, but volatility will become more intense, and asset selection will be key to becoming a market winner.

The bull market may continue for some time, but volatility will become more intense, and asset selection will be the key to becoming a market winner.

Written by: arndxt

Translated by: AididiaoJP, Foresight News

The view that the economy is reaccelerating is actually quite one-sided. Currently, it is mainly supported by the assets of wealthy households and investments driven by artificial intelligence. For investors, you cannot simply expect a broad market rally in this cycle:

- The core of long-term growth lies in semiconductors and AI infrastructure.

- Increase holdings of scarce physical assets: gold, metals, and certain promising real estate markets.

- Remain cautious about broad-based indices: the high concentration of the "Magnificent Seven" in the US stock market masks the overall fragility of the market.

- Closely monitor the trend of the US dollar: its direction will determine whether this cycle continues or is interrupted.

Just like from 1998 to 2000, the bull market may continue for a while, but volatility will become more intense, and asset selection will be the key to becoming a market winner.

Economic Divergence

Market performance is a true reflection of the economy. As long as the stock market remains near historical highs, claims of an economic recession are hard to believe.

We are currently in a clearly divergent economic environment:

- The top 10% income group contributes over 60% of consumption, accumulating wealth through stocks and real estate.

- Meanwhile, inflation continues to erode the purchasing power of low- and middle-income households. This widening gap explains why, on one hand, the economy is "reaccelerating," while on the other hand, the job market remains weak and the cost-of-living crisis persists.

Uncertainty Brought by Federal Reserve Policy

Be prepared for policy volatility. The Federal Reserve must address the appearance of inflation while also considering the political cycle. This creates opportunities, but it also means that if market expectations change, there could be a sudden risk of a downturn.

The Federal Reserve is currently in a dilemma:

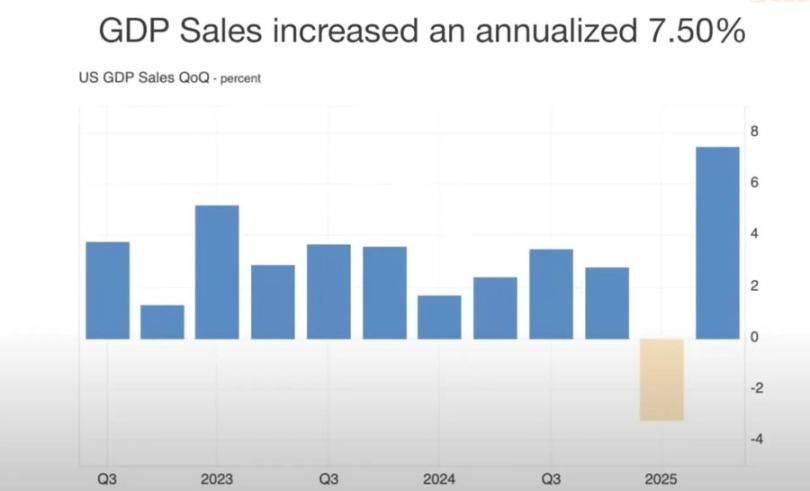

- On one hand, strong GDP growth and resilient consumption support a slower pace of rate cuts;

- On the other hand, high market valuations mean that delaying rate cuts could trigger "growth concerns."

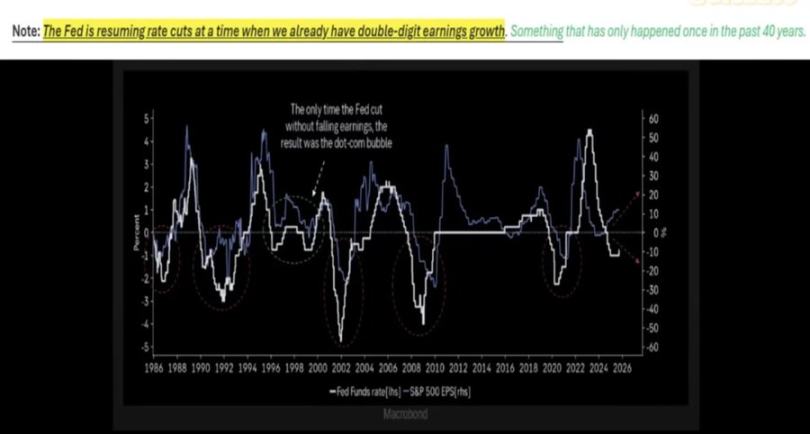

Historical experience shows that cutting rates during periods of strong earnings (such as in 1998) can extend a bull market. But this time is different: inflation remains stubborn, the "Magnificent Seven" in the US stock market have outstanding earnings, while the other 493 companies in the S&P 500 are performing mediocrely.

Asset Selection in a Nominal Growth Environment

One should hold scarce physical assets (gold, key commodities, real estate in supply-constrained areas) and sectors representing productivity (AI infrastructure, semiconductors), while avoiding excessive concentration in stocks hyped by online trends.

The coming period is unlikely to see a broad-based boom, but rather localized bull markets:

- Semiconductors remain at the core of AI infrastructure, with related investments continuing to drive growth.

- Gold and physical assets are once again demonstrating their value as hedges against currency depreciation.

- Cryptocurrencies are currently facing deleveraging and pressure from a surplus of US Treasuries, but structurally, they are closely related to the liquidity cycle that is driving gold higher.

Real Estate and Consumption Dynamics

If real estate and the stock market weaken simultaneously, the "wealth effect" supporting consumption will be impacted.

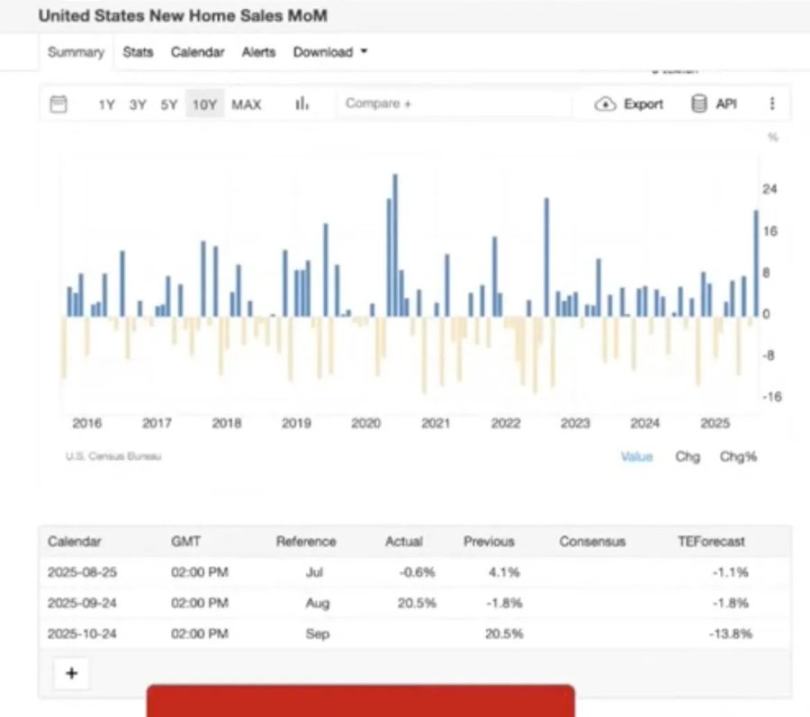

Real estate may see a brief rebound when interest rates are slightly lowered, but deeper issues remain:

- Supply and demand imbalances caused by demographic changes;

- Rising default rates due to the end of student loan and mortgage forbearance periods;

- Significant regional differences (older groups have asset buffers, while young families are under heavy pressure).

US Dollar Liquidity and Global Positioning

The US dollar is the key factor affecting the whole picture. If the global economy weakens and the dollar strengthens, more fragile markets may encounter problems before the US does.

An overlooked risk is the contraction of dollar supply:

- Tariff policies reduce the trade deficit, limiting the scale of dollar flows back into US assets;

- The fiscal deficit remains high, but foreign buyers are less interested in US Treasuries, which could trigger liquidity issues.

- Futures market data shows that short positions on the dollar have reached historical extremes, which could trigger a dollar short squeeze and undermine the stability of risk assets.

Political Economy and Market Psychology

We are in the late stage of the financialization cycle:

- Policymakers strive to "maintain the status quo" until key political milestones (such as general elections and midterms) have passed;

- Structural inequality (rents rising faster than wages, wealth concentrated among the elderly) fuels populist pressures, prompting policy adjustments in areas such as education and housing;

- The market itself is reflexive: capital is highly concentrated in seven large-cap stocks, which both supports valuations and sows the seeds of fragility.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

InnoBlock 2025 Successfully Concludes: Foreseeing the Next Journey of Web3

The InnoBlock 2025 conference focuses on the mainstream adoption of Web3, exploring cutting-edge topics such as stablecoins, AI, and RWA. The event brings together global industry leaders to promote cross-sector collaboration and technological innovation. Summary generated by Mars AI This summary is generated by the Mars AI model, and the accuracy and completeness of the content are still in the process of iterative improvement.

Bitcoin surges to two-week high on weak September jobs data, Fed rate cut bets

The US September ADP employment unexpectedly recorded a negative value, strengthening expectations of a Federal Reserve rate cut.

U.S. ADP employment in September posted the largest decline since March 2023, with the previous figure also revised to negative growth. As the release of the non-farm payroll report is likely to be delayed, the "mini non-farm" data may carry additional significance in guiding the Federal Reserve's October meeting.

Why can AC's new product Flying Tulip raise 1 billion dollars?

This article introduces Lemniscap's seed round investment logic in Andre Cronje's new project Flying Tulip, with a focus on its disruptive fundraising model and ambition to build a full-stack trading platform.